New Risk Element Analysis Pure Electric Vehicle

Written by: Bill Gao and Liu, Jianjun, Genilex

Preamble

We’re living in an era of rapid evolution of vehicle technology, ownership and usage. As a data and analytics expert in China's insurance industry, Genilex and its parent company LexisNexis Risk Solutions research and utilize international motor insurance operational data, as well as practical experience from the China market, to quantify the possible impact of new elements of vehicle risk on China's auto insurance market. We will be sharing Genilex’s research and insight with the auto insurance industry in a series of articles, looking at trends in new energy technology, Advanced Driver Assistance Systems (ADAS) and auto pilot technology, ride-sharing cars, used cars, car history and much more.

Let’s start with a discussion of new energy vehicles, focusing on changing risks associated with pure electric vehicles. We have analyzed the differences between pure electric vehicles and gas fueled vehicles for millions of historical policies and claims data in the U.S. market. This data, combined with the current Chinese auto insurance market, suggests the need for further refinement of pure electric vehicle underwriting risk segmentation for China's auto insurance industry.

Overview of New Energy Vehicle Development

In recent years, due to the government's subsidy policy, China’s fleet of new energy vehicles has grown rapidly. Following development trends, China’s pure electric vehicles and hydrogen fuel cell vehicles are forecast to lead the new energy vehicle market in China.

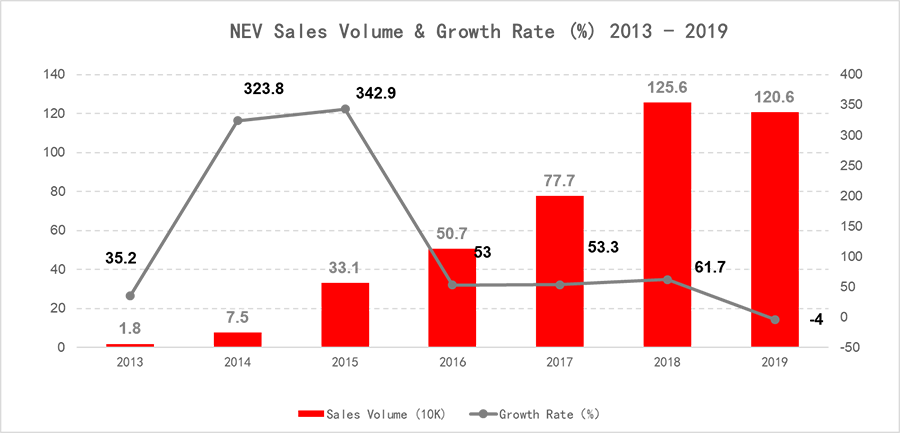

From 2013 to 2018, new energy vehicle production and sales increased annually in China. According to China Automobile Association statistics, By the end of 2019, the number of new energy vehicles produced nationwide reached 3.81 million, accounting for 1.46% of the total number of vehicles. Compared to the end of 2018, this represents an increase of 1.2 million vehicles and a 46% rise in this vehicle type. Among the total, there were 3.1 million pure electric vehicles at year-end 2019, accounting for 81% of new energy vehicles. New energy vehicle purchases have exceeded one million for two consecutive years, showing a rapid growth trend.

However, impacted by the decline of new energy vehicle subsidies, sales of new energy vehicles in the second half of 2019 showed a sharp decline. In 2019, China’s new energy vehicle sales were 1.206 million units, a 4% decrease from 2018. In 2020, COVID-19 caused the sales of new energy vehicles in China to fall sharply again. To support continuous development of the new energy vehicle industry, in April 2020, the Ministry of Finance, Ministry of Industry and Information, the Ministry of Science and Technology, and the Development and Reform Commission jointly issued the "Notice on Improving the Application of Financial Subsidy Policies for the Promotion and Application of New Energy Vehicles." This notice further clarified the timing and coverage of the promotion and application of financial subsidy policies for new energy vehicles over the subsequent two years. The new energy vehicle purchase subsidy policy that expired at the end of 2020 was to be extended for two years. At the same time, the intensity and pace of the subsidy reduction was to taper off more slowly. In principle, the subsidy standards for 2020-2022 have been set at 10%, 20%, and 30% annual reductions based on each previous year. 1

Challenges and opportunities in the insurance market

With the rapid development of the new energy vehicle industry, both insurers and drivers are raising concerns about new energy vehicles in terms of risk pricing and claim adjustment standards. Compared with traditional internal combustion engine (ICE) cars, new energy vehicles bring big differences in terms of costs for specific technologies, configuration of physical properties and power train principles. Together with cruising range anxiety, battery safety, and charging facilities’ availability, this vehicle revolution has brought many challenges to consumers and auto insurance carriers.

The risk trends between different new energy models are new challenges for the auto insurance industry. It is important to understand the characteristics of new energy vehicles and their underwriting risks, as well as how to reasonably quantify the risk differences between new energy and ICE vehicles. The U.S. auto insurance market has been working to gather experience and data on pure electric vehicle insurance.

Genilex has concluded the following risk differences between pure electric vehicles and ICE or gas vehicles, as well as the differences between pure electric vehicle types.

The methodology is based on an in-depth understanding of the Chinese insurance market, through researching the physical properties of batteries and electric motors of varied pure electric vehicle models, and analyzing the sampled U.S. auto insurance data (policy year from 2015 to 2019, covering about 820,000 car years for pure electric vehicle policies and 2.35 million car years for ICE vehicles).

Comparisons and considerations of the difference between pure electric vehicles and gas vehicles

1. To support a longer cruising range, light and high-strength materials such as ultra-high-strength steel, aluminum alloy, and carbon fiber material are adopted by most pure electric vehicle manufacturers. For example, the BMW i3 uses an all-carbon fiber body with an aluminum alloy chassis. Tesla uses aluminum alloy for both. However, these expensive spare parts drive a higher maintenance and repair cost compared to traditional ICE vehicles, resulting in higher claims severity.

2. The physical structure and core components of pure electric vehicles, such as battery pack, electric motors in the power train, electronic control system and so on, are associated with unusual risks (such as fire) and potential impact damage, which are significantly different from traditional ICE vehicles. Moreover, the new power systems (the battery pack) of pure electric vehicles create technical barriers in repair. This consequently leads to higher cost of restoring value from the insurance claim compared to ICE vehicles. Pure electric vehicles use a pack of thousands of battery cells that can be displaced in different parts of the vehicle. Capacities of battery packs vary but the typical replacement cost for premium vehicles has been estimated at $10,000 or ¥ 60,000 in 2021.

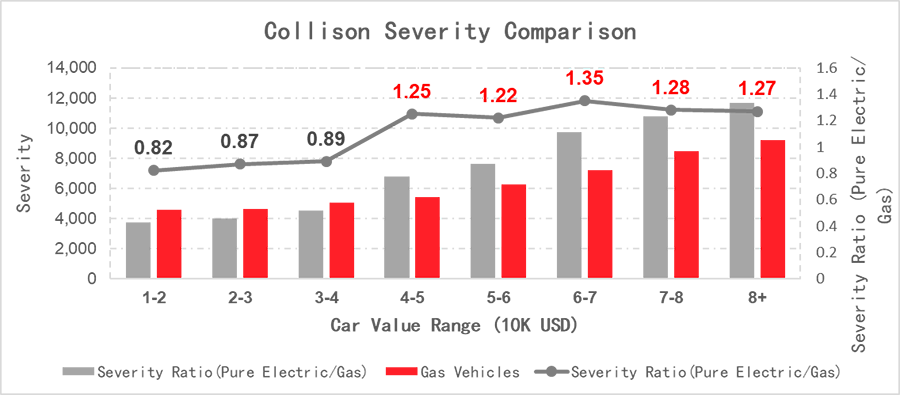

Genilex concluded that pure electric vehicles have higher underwriting risk compared to ICE vehicles after analyzing the sampled U.S. auto insurance market data. The collision severity is about 30% higher compared to ICE vehicles. The difference is most severely reflected for mid-to-high priced models (≥ $40,000).

The lower purchase prices of pure electric vehicle models due to government subsidies (national and local), the un-unified measurement of battery pack performance decay, and the lack of standardized repairing guidelines are all causing the residual values to be inaccurately determined. These factors will probably result in higher reputational risk and higher reputational risk for pure electric vehicle coverage, compared to ICE vehicles in terms of collision coverage.

3. Electric motors have greatly reduced noise levels compared to traditional engines. This can increase personal injury risk for pedestrians if it alters their general perception of nearby traffic. Therefore, this could cause higher claims frequency from third party liability coverage, compared to ICE vehicles.

4. Pure electric vehicles have large regional differences in performance. Because battery performance is significantly affected by temperature, there are very few pure electric vehicles in northern China. However, the rainy climate in the south is also a major challenge for battery protection and sealing. In recent years, damage claims arising from short circuit and overheating due to water inflow caused by heavy rain have become common.

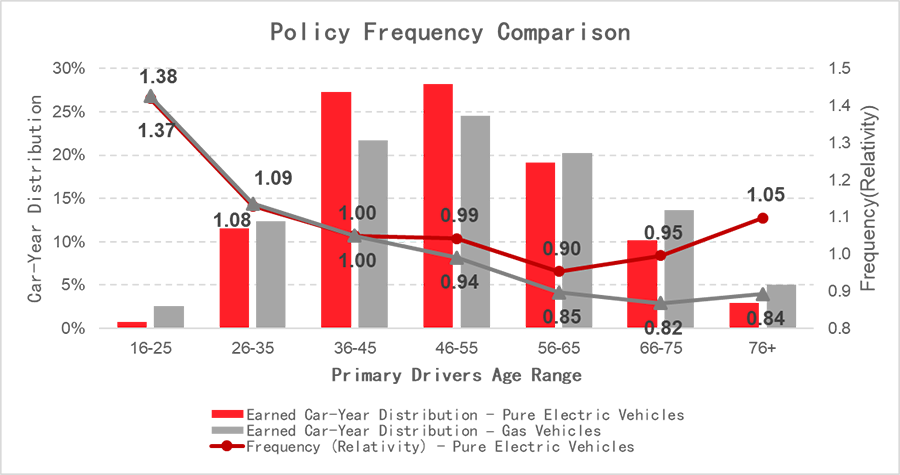

5. There are significant risk differences among different ages of primary drivers between pure electric vehicles and ICE vehicles. As shown in the following chart, in the U.S. market, the frequency relativity of the primary drivers over the age of 45 driving pure electric vehicles is significantly higher than those of ICE vehicles. The majority of pure electric vehicle drivers are in the age range of 36 to 55. However, in the China market, due to ICE vehicle licensing control in the major cities and a series of government incentive policies on pure electric vehicles, the owner population of pure electric vehicles in cities is younger. We can also see in the chart below that the frequency relativity for young drivers, under 35 years old, especially under 25 years old, is much higher than that of more mature drivers for both pure electric vehicles and ICE vehicles.

Comparison and consideration of differences between pure electric vehicles

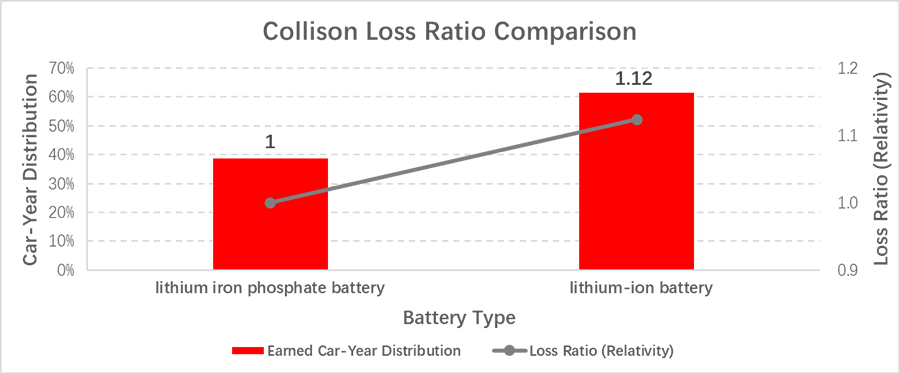

1. There are many types of batteries for pure electric vehicles, such as ternary lithium manganate composite battery, ternary nickel cobalt manganese lithium battery, ternary lithium battery, lithium iron phosphate battery, nickel cobalt manganese lithium battery, lead acid battery, lithium-ion battery, amongst others. The capacities of the battery power storage can range from 10KWh to 435KWh. Most domestic vehicles in China use lithium iron phosphate batteries for stability of operation and for ordinary power output (accounting for nearly half of the current market). The imported electric vehicles represented by Tesla choose high-performance and relatively active lithium-ion batteries. Through data analysis, Genilex found that the average battery capacity of imported pure electric vehicles is about 1.7 times that of the domestic pure electric vehicles, and the cruising range is about 1.6 times that of the domestic pure electric vehicles. However, the collision loss ratio relativity differs by more than 10% between these two types of batteries.

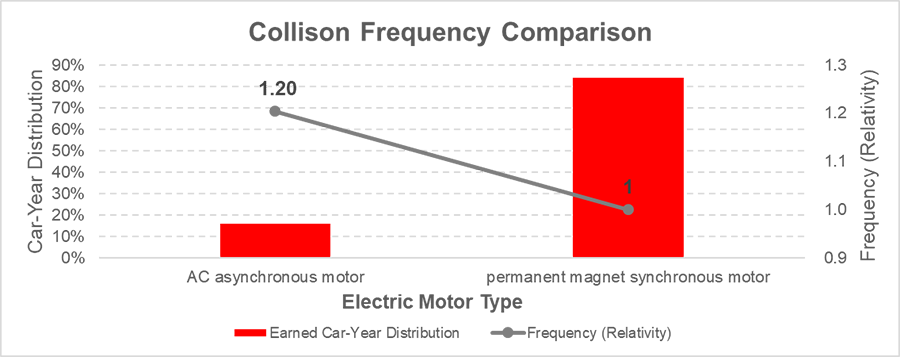

2. Electric motor performance also varies significantly. Most domestic electric vehicles use permanent magnet synchronous motors with a price advantage. But about 65% of imported vehicles use high-power AC asynchronous motors. Through data analysis, Genilex found that the average power of an AC asynchronous motor is about 4.3 times of a permanent magnet synchronous motor, and roughly 2.4 times more in average torque. In addition, the electric motors in a vehicle can be allocated to the front axle, rear axle or both (all-wheel drive). Therefore, the horsepower and torque differ widely among pure electric vehicle types. Stronger power leads to greater acceleration performance but it also correlates to a higher rate of collisions and claims. The analysis below shows the collision frequency relativity of pure electric vehicles with AC asynchronous motors is more than 15% higher than those with permanent magnet synchronous motors.

Analysis of the auto insurance data in the U.S. showed there is also a large difference in collision frequency among pure electric vehicle types.

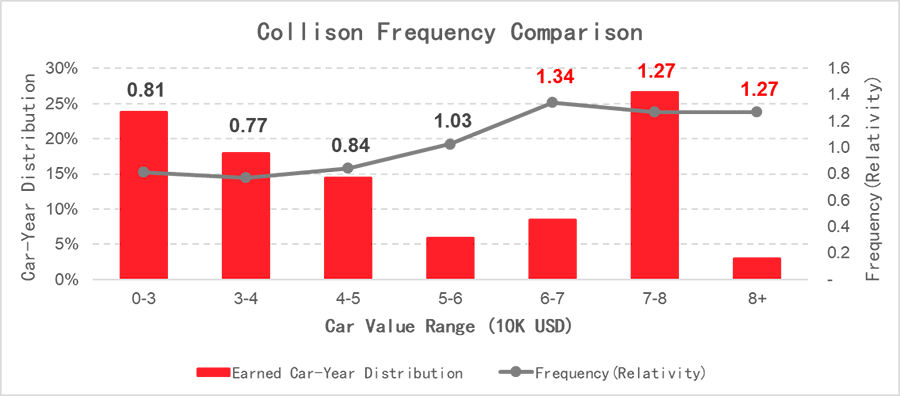

3. The more expensive pure electric vehicles (average price of $60,000 and above) have about 48% higher collision frequency than the cheaper models.

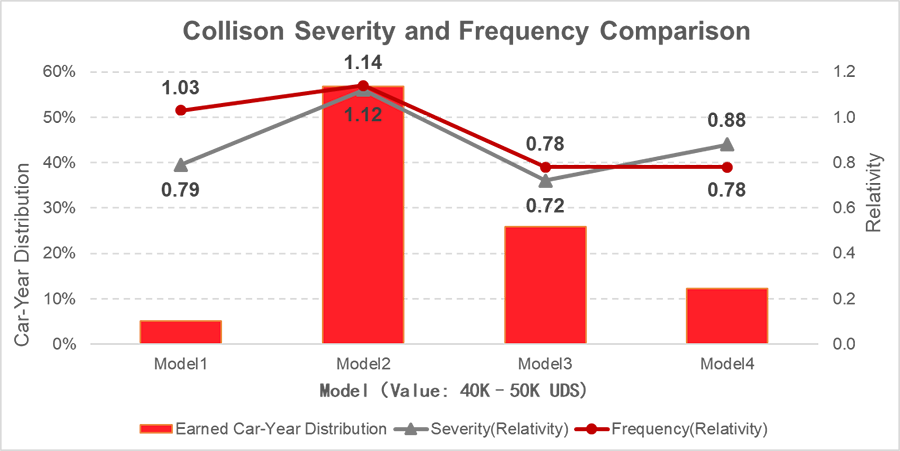

At the slightly lower price range ($40,000 to $50,000), certain models have about 46% higher collision frequency than other cheaper models. And their average collision severity is about 43% higher than cheaper models.

Summary

This Genilex and LexisNexis analysis shows there are significant differences in risks and loss cost frequency between pure electric vehicles and ICE vehicles, when comparing both physical vehicle characteristics and insurance data. Moreover, the physical property differences between different pure electric models can also be proven by this data investigation.

In China, the exclusive pure electric vehicle insurance product is still in the research and development phase. The current premium rates and coverage terms are developed for specifically for ICE vehicles. Without a large volume of historical data for China and mature operating experience, Genilex recommends the following two aspects to improve the risk segmentation and refinement in underwriting of pure electric vehicles:

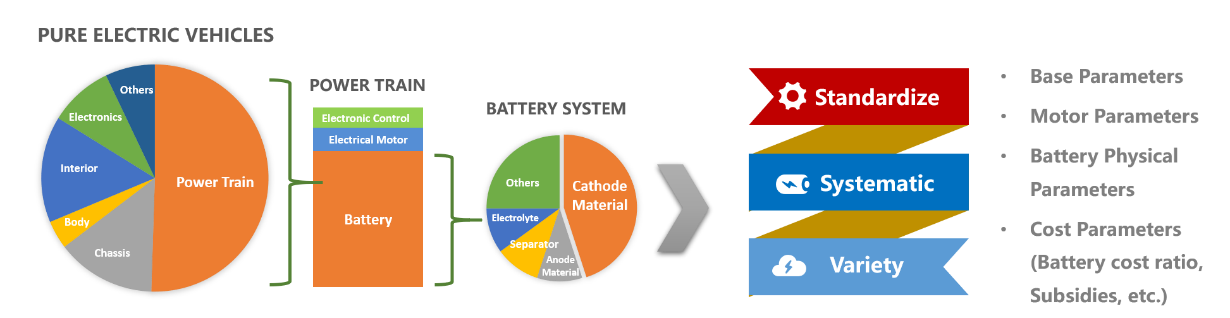

1. Collect and standardize risk characteristics of varied domestic and imported pure electric vehicles.

2. Build an initial risk segmentation and underwriting model based on international insurance operational experience specifically from pure electric vehicles. Promptly and rapidly improve the model with more and more local insurance data.

It’s the insurance carrier’s responsibility to accurately price the unique risks for new vehicle types and even to develop exclusive products for pure electric vehicles. This is going to require deep understanding of the changing nature of risk, and developing new measurements for driving the market, to keep the industry operating at high efficiency.

1Resource: Market Status and Development Trend Analysis of 2020 China Pure Electric Vehicles Industry-New Policy Favorable to Sector Development

https://www.qianzhan.com/analyst/detail/220/200511-e263435a.html