Press Room

LexisNexis Insurance Demand Meter Registers as “Sizzling” for New Policies and “Hot” for U.S. Auto Insurance Shopping

08/16/2023

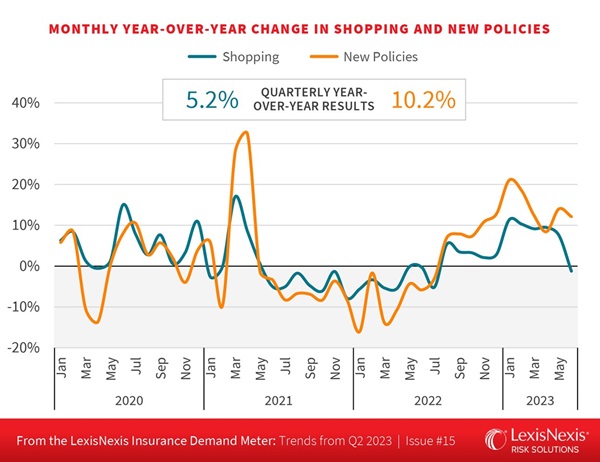

ATLANTA — The latest edition of the LexisNexis® Risk Solutions Insurance Demand Meter reports the quarterly year-over-year U.S. auto insurance shopping growth was +5.2% in Q2 2023, as consumers continue to react to widespread rate increases by auto insurers in the face of an ever-hardening market. Although year-over-year shopping growth remains high, new business volumes began to outpace shopping last quarter, signaling that the consumers that are shopping are finding policies that suit their individual needs. Quarterly year-over-year new policy growth, or the rate at which consumers either switched or purchased new coverage –– was strong at +10.2%.

“Profitability is still a challenge for many insurers, driven in large part by a continued rise in claims severity across the market associated with rising costs to repair damaged vehicles,” said Adam Pichon, senior vice president of auto insurance and claims at LexisNexis Risk Solutions. “As a result, most carriers are being much more discerning in their underwriting processes and cutting back on marketing spend, but motivated shoppers still sought better cost savings, and switched their policies in record numbers in May and June.”

Claims Severities Create a Bumpy Road to Profitability

Increased claims severities have continued to challenge the U.S. auto insurance market, registering six consecutive quarters of at least 5% growthi. Fueled by labor and part shortages, the cost to repair – or replace – vehicles is increasing, and more than a quarter of collision events from 2022 (27%) were total lossesii, which has added more expense pressure. Insurers are reacting accordingly, not only by taking rate and reducing marketing spend, but some large carriers have even pulled out of higher-risk markets altogether.

“It’s a tough situation. Inflationary pressure on repair costs is creating more total losses on top of the added costs to those vehicles that can be repaired – and our data continues to suggest that consumers are shopping near claims events,” said Chris Rice, associate vice president of insurance strategic business intelligence, LexisNexis Risk Solutions. “When you combine these macroeconomic factors with claims and injury severities soaring, a lot of insurers have taken a step back to reassess how they will manage risk across their books of business for the foreseeable future.”

How are Consumers Responding? Shopping for Cost Savings… and Policy Consolidation

Many insurance carriers have responded conservatively to the current hard market. Lower cost policies may be difficult to find, but savvy shoppers are still finding them, leading to very high new policy growth numbers in recent quarters. But new policy growth is only part of the consumer story.

While new policy volumes remain on the rise, U.S. auto policies’ in-force growth has slowed below traditional averages. This trend is not solely attributable to drivers leaving the market or driving uninsured. The latest version of the Insurance Demand Meter suggests the largest cause of this discrepancy is linked to household consolidation as more drivers, such as adult children moving back in with parents or relatives to save money or take on additional responsibilities for the household, are being added to existing policies. In fact, the Demand Meter analysis points to as many as 2.4 million fewer policies in the market over the second quarter due to household consolidation.

A Look Ahead

Pichon also advises to keep a close eye on the property insurance market, which may be following the auto insurance market’s lead in raising rates.

“We indicated in previous editions of the Demand Meter that there would be an opening for opportunistic shoppers to find cost savings when shopping for auto insurance this year, and that was certainly the case,” said Pichon. “But how long can certain carriers that have been slower to take rate afford not to do so at the scale of some of their competitors? Now, we are seeing some similar rate-taking activity on the property insurance side of the equation, which could be another key factor that drives shopping over the remainder of the year.”

“A lot of carriers are gearing up for the next round of rate increases,” continued Pichon. “How consumers respond with respect to shopping in Q3, including how many more might exit the market, should give us a pretty good look at what 2024 may hold.”

Download the latest Insurance Demand Meter.

About the LexisNexis Insurance Demand Meter

The LexisNexis Insurance Demand Meter is a quarterly analysis of shopping volume and frequency, new business volume and related data points. LexisNexis Risk Solutions offers this unique market-wide perspective of consumer shopping and switching behavior based on its analysis of billions of consumer shopping transactions since 2009, representing nearly 90% of the universe of insurance shopping activity.

About LexisNexis Risk Solutions

LexisNexis® Risk Solutions provides customers with information-based analytics and decision tools that combine public and industry-specific content with advanced technology and algorithms to assist them in evaluating and predicting risk and enhancing operational efficiency. Headquartered in metro Atlanta, Georgia, the company has offices throughout the world, serves customers in more than 190 countries and territories and is part of RELX. For more information, please visit LexisNexis Risk Solutions and RELX.

iLexisNexis Risk Solutions Internal Data

iiLexisNexis Risk Solutions Internal Data

Media Contacts

Sr. Director, Communications

Insurance and Connected Car and Coplogic Solutions

[email protected]

+1.678.896.1463