Press Room

LexisNexis Insurance Demand Meter Shows Third Consecutive Quarter of Negative Growth in U.S. Auto Insurance Shopping Rates

05/24/2022

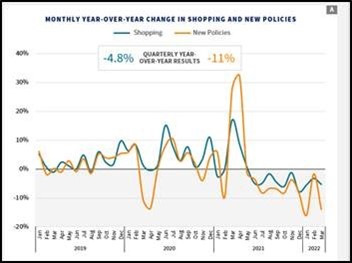

ATLANTA — The latest edition of the LexisNexis® Risk Solutions Insurance Demand Meter reports the overall annual U.S. auto insurance shopping growth rate, which includes shopping and new policies, dropped for the third consecutive quarter for the first time since LexisNexis Risk Solutions began releasing these quarterly metrics. Shopping was down 4.8% in Q1 2022 versus Q1 2021 – compared to -5.2% in Q4 2021 versus Q4 2020 – as the industry continues to grapple with increased claims costs and a 16% decline in new car sales from a year ago.

New policy growth declined 11% for the quarter versus Q1 2021 as insurers scaled back marketing spend, and consumers were forced to account for early dispersal of half of the child tax credit. However, some of that decline year over year can likely be attributed to the fact that Q1 2021 saw higher than normal seasonal shopping, which was boosted by the final round of stimulus checks from the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

“The auto insurance and automotive OEM industries are still facing significant headwinds related to decreased marketing spend by carriers, variables in tax refunds for consumers, and new and used vehicle shortages, but I don’t think it’s time to sound the alarm just yet,” said Adam Pichon, vice president and general manager, auto insurance, LexisNexis Risk Solutions. “The market is still reacting to pandemic-related and macroeconomic factors such as chip shortages, inflation, and labor shortages, and carriers are responding to claims inflation challenges by raising rates. Rate taking among carriers is expected to continue through 2023, which will likely drive consumers back into the insurance shopping market.”

With Claims Severity Up, Carriers’ Marketing Spend is Down

As reported in last quarter’s edition of the Insurance Demand Meter as well as the newly released 2022 Auto Trends Report, suppressed new vehicle sales persisted into Q1 2022 and were down 16% from the year prior. This lack of automotive inventory has also created a ripple effect in driving up used vehicle prices. As a result of more vehicles on the road and the aging car park, insurance claim severities have been on the rise, particularly for total losses.

With an eye on profitability, many insurers have drastically cut their marketing spendi. This is having a significant impact, especially in the direct channel where corporate marketing is critical to creating new insurance shoppers. LexisNexis Risk Solutions analysis suggests shopping volumes are down 3% or more due to reduced spend on direct mail marketing alone.

Uncertainty Swirls Due to Variances in Tax Return Shopping

New shopping volumes for uninsured drivers who qualify for the Earned Tax Creditii (EITC) and the Additional Child Tax Creditiii were down in Q1 2022, as they were a year ago during the same period. This marks a two-year divergence from the typical pre-pandemic pattern we typically see in our data during tax season.

While the early disbursement of the Additional Child Tax Credit in late 2021 did not appear to have a significant impact on the depressed shopping volumes among the uninsured segment, it did impact the overall shopping volumes across all demographics.

Insurers Respond – and a Look Ahead

As expected, rate filings were a priority among carriers in Q1 2022, and that should continue for at least the next 18 months.

“Upticks in claim frequency and severity have forced the hand of insurers to revisit rate adequacy,” said Pichon. “We will continue to keep a close eye on the auto insurance market’s rate activity and gauge whether it becomes a key catalyst for increased U.S. consumer shopping when they see their premiums are higher.”

Download the latest Insurance Demand Meter.

About the LexisNexis Insurance Demand Meter

The LexisNexis Insurance Demand Meter is a quarterly analysis of shopping volume and frequency, new business volume and related data points. LexisNexis Risk Solutions offers this unique market-wide perspective of consumer shopping and switching behavior based on its analysis of billions of consumer shopping transactions since 2009, representing nearly 90% of the universe of insurance shopping activity.

About LexisNexis Risk Solutions

LexisNexis® Risk Solutions provides customers with information-based analytics and decision tools that combine public and industry-specific content with advanced technology and algorithms to assist them in evaluating and predicting risk and enhancing operational efficiency. Headquartered in metro Atlanta, Georgia, the company has offices throughout the world, serves customers in more than 190 countries and territories and is part of RELX. For more information, please visit LexisNexis Risk Solutions and RELX.

i https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/geico-progressive-break-trend-slash-advertising-expenditures-in-2021-69764365 and Q1 2022 Personal Lines Overview, Competiscan, ©2022.

ii www.eitc.irs.gov/partner-toolkit/basic-marketing-communication-materials/eitc-fast-facts/eitc-fast-facts

iii www.irs.gov/credits-deductions/ individuals/earned-income-tax-credit/earned-income-tax-credit-statistics

Media Contacts

Sr. Director, Communications

Insurance and Connected Car and Coplogic Solutions

[email protected]

+1.678.896.1463