Press Room

U.S. Consumers Continue to Shop and Switch Auto Insurance at Higher Rates, Dragging Down Carriers’ Retention Rates

02/21/2024

ATLANTA

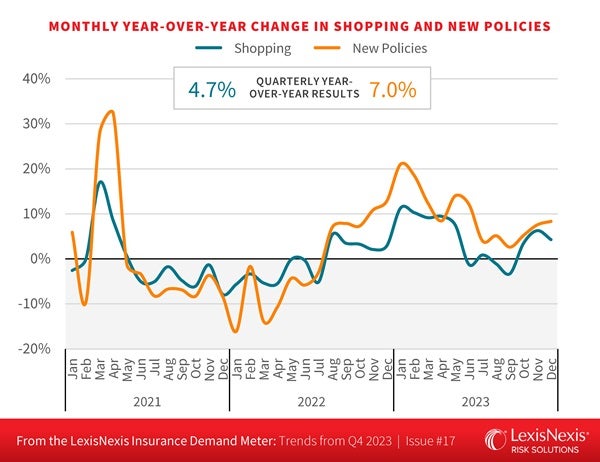

Key takeaways- U.S. auto insurance shopping and new policies posted positive year-over-year growth and record volumes for the final quarter of the year, both registering as ‘Hot’ on the LexisNexis® Insurance Demand Meter.

- Year-over-year shopper growth showed the strongest Q4 growth since 2020.

- Quarterly year-over-year growth for new policies outpaced shopper growth for the sixth consecutive quarter, meaning consumers continue to switch carriers at an increasing rate when they shop.

- Not resigned to higher rates, 41% of insured households shopped their auto insurance at least once in 2023.

- Retention levels have dropped a staggering three percentage points since Q1 2022 as consumers hit the market

- In an already “hot” shopping market, consumers actively shopped their auto insurance policies.

- Year-over-year shopper growth rebounded from -1.2% in Q3 to 4.7% in Q4.

- Quarterly year-over-year growth for new policies rose from 3.9% to 7.0%

- Overall, shopping and new business volumes exploded in the first months of the year, as rate increases impacted the market.

- Claims costs, inflated vehicle repair costs and unfavorable reserve development slowed growth by detracting from profitability gains.

- Insurers walked back new customer acquisition efforts during the summer, resulting in a short-lived dip in shopping in Q3.

- In Q4, activity bounced back, brought on by elevated rates and increased market efforts, creating prime conditions for a hot market.

- In the final quarter of the year, insurer marketing spend, particularly in the direct distribution channel, increased shopping and switching and brought the year-over-year annual policy growth to 9.8%.

“As the industry sees rates spike and expands marketing to prime consumers for increased shopping, it will be key to observe activity on a state-by-state level,” said Adam Pichon, senior vice president, U.S auto and claims, LexisNexis® Risk Solutions. “When we look at Texas, a leading state for improved profitability, both the number and size of rate increases have dwindled. While we can’t predict the shopping trajectory for states still looking to achieve rate adequacy, we will watch closely to determine whether Texas can serve as a bellwether for the rest of the country.”

Direct distribution stages a comeback with increased market activity.As market dynamics shift, the direct distribution channel single-handedly drove Q4 growth. This sits in contrast to the previous quarter when independent agents zeroed in on consumer desires to shop policies from multiple carriers.

- Direct distribution channel growth exploded, increasing by 27%.

- The direct distribution channel offset the negative growth in the agent-based channels.

Twelve of the 15 fastest-growing states are located in the West and Midwest regions.

- Across the U.S., 39 states saw positive growth; of that, 15 experienced double-digit growth.

- Top-performing states for shopping growth included: Hawaii (67%), West Virginia (44%), Iowa (41%), South Dakota (29%) and Utah (23%).

- States that saw negative growth year-over-year included Washington D.C. (-15%), Oklahoma and New York (-7%), Rhode Island (-6%), New Hampshire (-5%) and Texas (-4%).

With 2024 already underway, insurers have an opportunity to seize market share, particularly evident in the direct channel where factors like marketing expenditure and rate adjustments are prompting increased shopping behavior. Texas, one of the first states to increase rates and experience positive growth, saw negative shopping numbers in the final quarter of 2023. This may highlight the need for insurers to adapt their strategies and balance acquisition with rate competitiveness to capitalize on increased shopping before it stabilizes. While there’s a window of opportunity, it may be temporary. Insurers may only have a limited timeframe to take advantage of current insurance industry conditions and secure their market position.

“With profitability top of mind in 2024, we expect to see many insurers taking a closer look at their portfolios and in some cases re-underwriting certain policies,” said Pichon. “This could yield continued increases in shopping as consumers seek the most affordable policies.”

Download the latest Insurance Demand Meter.

LexisNexis Insurance Demand MeterThe LexisNexis® Insurance Demand Meter is a quarterly analysis of shopping volume and frequency, new business volume and related data points. LexisNexis Risk Solutions offers this unique market-wide perspective of consumer shopping and switching behavior based on its analysis of billions of consumer shopping transactions since 2009, representing nearly 90% of the universe of insurance shopping activity.

About LexisNexis Risk Solutions

LexisNexis® Risk Solutions provides customers with information-based analytics and decision tools that combine public and industry-specific content with advanced technology and algorithms to assist them in evaluating and predicting risk and enhancing operational efficiency. Headquartered in metro Atlanta, Georgia, the company has offices throughout the world, serves customers in more than 190 countries and territories and is part of RELX. For more information, please visit LexisNexis Risk Solutions and RELX.

Media Contacts

Sr. Director, Communications

Insurance and Connected Car and Coplogic Solutions

[email protected]

+1.678.896.1463