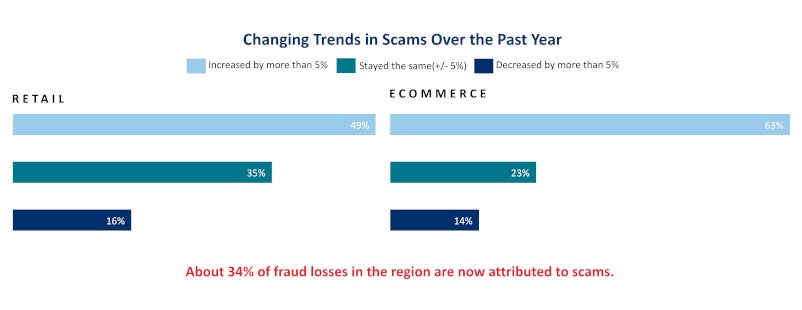

Discover how retail and ecommerce merchants in North America are protecting customers and transactions from sophisticated identity fraud.

In the latest LexisNexis® True Cost of Fraud™ study, merchants share widespread confidence in fraud prevention processes despite critical challenges:

-

The average merchant spends $4.60 on each dollar lost to fraud — a 32% increase since 2022.

-

More than 40% of merchant organizations rely on manual fraud prevention processes.

-

Fraud prevention increases customer churn at 59% of U.S. merchants and 46% of Canadian merchants.

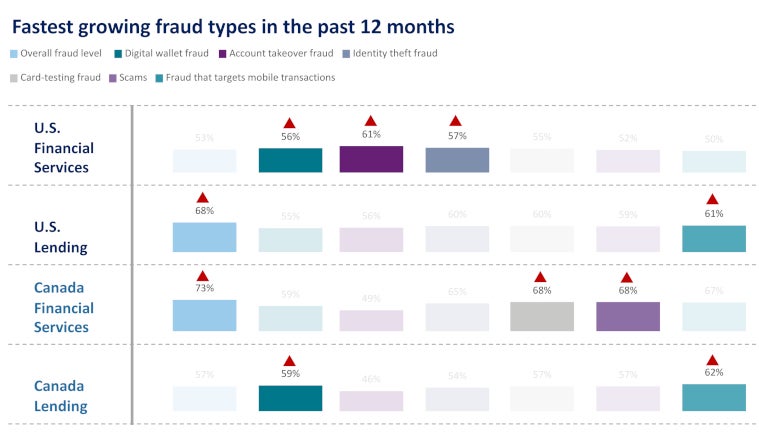

How are forward-thinking retail and ecommerce organizations increasing conversions and approvals while mitigating fraud losses across channels, payment methods and the customer journey?

To find out, download the study, and benchmark your retail or ecommerce business against responses from over 500 risk and fraud executives in the industry.

Additional Insights

LexisNexis and the Knowledge Burst logo are registered trademarks and LexisNexis Fraud Multiplier is a trademark of RELX Inc. True Cost of Fraud is a

trademark of LexisNexis Risk Solutions Inc. Other products and services may be trademarks or registered trademarks of their respective companies.

Copyright © 2025 LexisNexis Risk Solutions.

Products You May Be Interested In

-

BehavioSec®

Transform human interactions into actionable intelligence

Learn More -

Emailage®

Emailage® is a proven risk scoring solution to verify consumer identities and protect against fraud

Learn More -

FraudPoint®

Combat identity fraud with sophisticated scoring and leading analytics

Learn More -

Fraud Intelligence

Fraud Intelligence predicts the likelihood a new application will result in fraud

Learn More -

InstantID® Q&A

Authenticate customer identities in real-time

Learn More -

One Time Password

Authenticate a user with a one-time login transaction

Learn More -

Phone Finder

Connect phones and identities with rank-ordered results

Learn More -

ThreatMetrix®

Enable cybersecurity and risk management through data science innovation and shared intelligence

Learn More -

TrueID®

Recognize a true identity and fight fraud in real time

Learn More